American Cannabis News

No Reason to Own Curaleaf – New Cannabis Ventures

You are reading this week’s edition of New Cannabis Ventures, a weekly magazine we have published since October 2015. The newsletter includes unique insight to help our readers stay ahead of the curve, as well as links to the most important news of the week. We no longer email them like we used to, but post this and all newsletters on our website here.

friends,

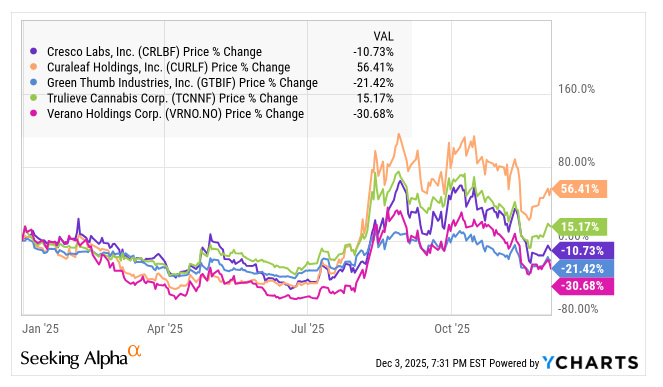

There hasn’t been much cannabis news this week, but what we did learn was kind of surprising. Cannabist, which sold one of its Virginia businesses to Verano for $90 million in 2024, announced the sale of its remaining Virginia assets to Curaleaf. Cannabist’s press release disclosed the price, while Curaleaf did not. Cannabist rallied and sold off and is now down 13.9% this week and down 39.9% year to date. The company is extremely difficult, in my opinion, and doesn’t really hold much value for investors given its low market cap and small trading volumes. Creditors are the ones who care.

Curaleaf, on the other hand, rallied on Wednesday after pulling back on Tuesday after announcing a pending $110 million buyout. It’s up 6.9% this week and is set to rise 56.4% in 2025. This is much better than the Global Hemp Stock Index, which is down 11.5% year-to-date at 6.09. MSOS, which carries most of Curaleaf, is down 3.2% in 2025.

I downgraded Curaleaf to Strong Sell at Seeking Alpha in April when it was $0.98 and yesterday it closed at $2.44. I remain very bearish on stocks and today I share an updated outlook. The main problems I see are that the valuation is too high relative to peers, the company has huge debt and MSOS has a lot.

Curaleaf’s rating is high compared to peers

While the current value of 7.8X projected adjusted EBITDA for 2026 may seem low, it is a large premium to its peers;

Curaleaf outperformed the major MSOs in 2025, driving this high relative valuation;

Curaleaf’s balance sheet is poor

The balance sheet is bad and getting worse. Net debt was $436 million at the end of 3Q, but most of the debt is due at the end of 2026, an amount that far outweighs cash. Management said on a conference call that it will replace it soon. That debt is currently realized at 8 percent cost. The company reported a current ratio of 1.5X. but that large debt due in 2026 will become current instead of long-term at the end of Q4 and this ratio will drop to 0.6X. The Virginia purchase would reduce it further.

Of course, the company can roll over the debt, but lenders should consider negative tangible equity as of Q3 of $853.6 million. This includes huge tax liabilities of $759 million. It is possible that the company will get a new loan, but investors should expect the interest rate to be potentially higher than the current 8%. The company may also sell some shares.

MSOS owns a lot of Curaleaf

MSOS controls 74.47 million shares of Curaleaf, its largest position. The Curaleaf has a thin flame compared to its peers and this further reduces it. Curaeaf’s shares are 678 million, so MSOS’s stake is more than 10% of the company’s outstanding subordinated shares, which trade over the counter in the US and on the TSX in Canada. I add the multiple voting shares as well as the RSUs and PSUs and some cash options to get a total stock dilution of 803 million, so MSOS has a 9.3% stake in the company.

If MSOS receives repayments again, it will likely need to sell more Curaleaf. Most investors remember the large number of ETF shares that redeemed in late 2022 and 2023. There were further redemptions in early 2025 and then again in November, when the number of shares fell 2%. Yesterday, shares fell by 0.5% due to another redemption. Despite this decline, the number of shares expanded by 41% in 2025. Curaleaf shares controlled by MSOS are up 54% year over year, compared to 32% for Trulieve and 2% for GTI. Curaleaf now holds the largest position at 26.7%, while Trulieve has 21.6% and Green Thumb Industries has 21.3%.

When MSOS received redemptions in November, it reduced Curaleaf shares it controlled by 2%, and then again yesterday. If the ETF receives more redemptions, it will likely sell more CURLF. This could be a problem if the ETF receives redemptions after bad news regarding 280E taxation emerges, as there are fewer buyers in that scenario.

Conclusion

Curaleaf traded at $0.84 on June 30 and rose to $2.04 on August 8, just ahead of the potential restructuring news. It’s unclear to me why Curaleaf is doing so well compared to its peers and other cannabis stocks. Cannabis stocks have been very volatile. Two that I have not liked at all over the past few years, Canopy Growth and Tilray Brands, have fallen so much and sold off the stock so much that I am now neutral on both. The demise of the 280E, if it happens, would be great for Curaleaf, but there are others that would benefit greatly as well. Investors looking to buy an MSO have better options than Curaleaf, which is quite risky.

Sincerely,

Alan:

New Cannabis Ventures publishes curated articles as well as exclusive news. Here is what we published last week.

Exclusives

Hemp stocks extend decline in November

M&A:

Cannabist to sell Virginia assets to Curaleaf

Follow Alan for real-time updates X.com:. Share and discover industry news with like-minded people on the largest group of cannabis investors and entrepreneurs LinkedIn:.

View: Public Hemp Company Revenue and Earnings Trackingwhich ranks the highest-earning hemp stocks.

Stay on top of the most important communications from public companies by watching what’s coming cannabis investor calendar.

Based in Houston, Alan leverages his experience as an online community founder 420 Investorthe first and still the largest due diligence platform focused on publicly traded stocks in the cannabis industry. With his extensive network in the cannabis community, Alan continues to find new ways to connect the industry and facilitate its sustainable growth. time New Cannabis Ventureshe is responsible for content development and strategic alliances. Before turning his attention to the cannabis industry in early 2013, Alan, who began his career on Wall Street in 1986, worked as an independent research analyst with more than two decades of research and portfolio management experience. A prolific writer, with over 650 articles published since 2007 Looking for Alphawhere he has 70,000 followers, Alan is a frequent speaker at industry conferences and frequent source Media including the NY Times, Wall Street Journal, Fox Business and Bloomberg TV. Contact Alan. Twitter: |: Facebook |: LinkedIn: |: El

You are reading this week’s edition of New Cannabis Ventures, a weekly magazine we have published since October 2015. The newsletter includes unique insight to help our readers stay ahead of the curve, as well as links to the most important news of the week. We no longer email them like we used to, but post this and all newsletters on our website here.

friends,

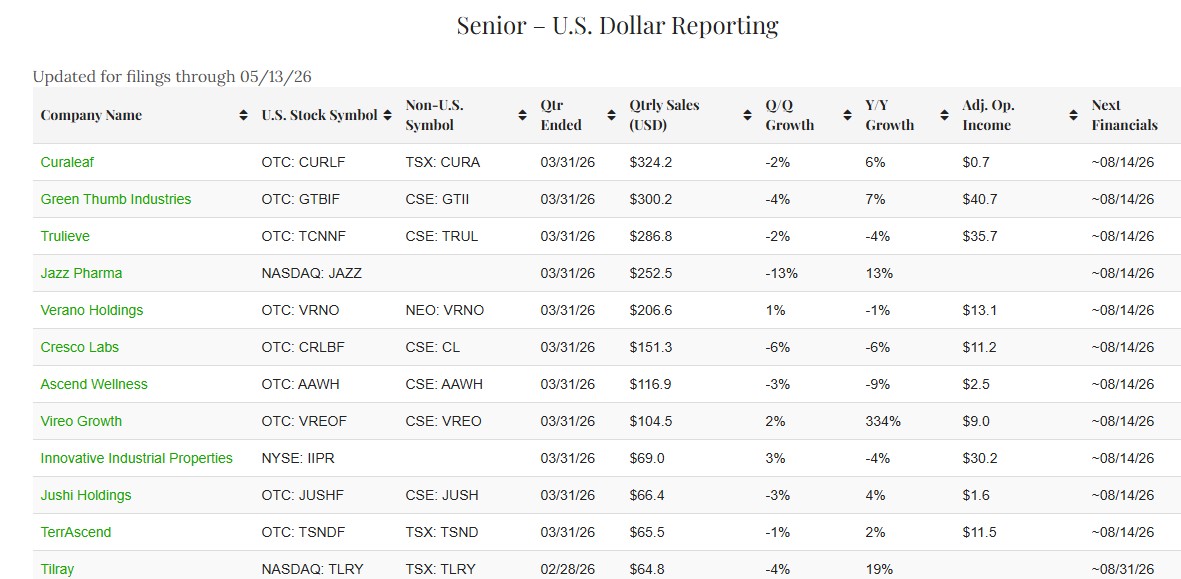

Many more cannabis companies reported Q1 financials this week. While NCV did not run any of those press releases, all data has been updated in the New Cannabis Ventures Public Cannabis Company Revenue & Income Tracker. The largest companies reporting in US dollars all reported, and the eleven companies that reported for the Q1 ended in March (excluding Tilray Brands, which is due to report its Q4 later this month) saw an average year-over-year revenue increase of 31% in their cannabis businesses.

Excluding Vireo Growth, that average comes to -0.7%, which is lower, especially after accounting for inflation, and a sign of continued challenges for the hemp industry. Speaking of Vireo, I’ve pointed out how investors didn’t care, and they still don’t. An average of just 375,000 shares traded per day over the past month, and the stock, which closed at $0.415, continues to trade off the level of its late 2024 capital raise and the price at which the company issued shares to make multiple acquisitions.

April was a big month for hemp stocks, but prices fell in May. The NCV Global Cannabis Stock Index rose 8.8% to 5.70 in April, but fell 2.8% to 5.54 in May. The year-to-year change of this index, which now covers 23 stocks, was -15.9%. Since its peak in early 2021, the GCSI is down 94%. Many are excited about the medical cannabis realignment that took place in April, although it remains unclear whether cannabis will be completely overhauled. The Department of Justice will hold hearings in late June to discuss adult-use cannabis, and it could be. If so, 280E tax would be removed, and this would be very good. I’ve written a lot about this since late 2022 when I highlighted it The potential end of 280E as a major catalyst.

The investor base in cannabis stocks has shrunk due to capital losses and fewer people interested in the sector. Institutions were more interested in high prices and maybe they would enter the field. 280E remains a big story, and not only is it being delayed by the limited realignment that’s already been completed, it’s unclear how unpaid taxes from the last few years will be treated.

NCV has stopped publishing most cannabis news, although we continue to update the financial calendar as well as the earnings rankings. After more than 10 years with NCV and more than a dozen years with 420 Investor, I am in the process of moving on. This is probably the last weekly newsletter. I’ve appreciated sharing the news and my views here, and I want to wish everyone the best. Hopefully, 280E taxation will be fully completed and the bear market that began in early 2021 for the hemp sector will be over.

Sincerely,

Alan:

Contact us acquire NCV assets or a website domain

New Cannabis Ventures publishes curated articles as well as exclusive news. Here is what we published last week.

Exclusives

Michigan cannabis sales are down again

View: Public Hemp Company Revenue and Earnings Trackingwhich ranks the highest-earning hemp stocks.

Stay on top of the most important communications from public companies by watching what’s coming cannabis investor calendar.

Based in Houston, Alan leverages his experience as an online community founder 420 Investorthe first and still the largest due diligence platform focused on publicly traded stocks in the cannabis industry. With his extensive network in the cannabis community, Alan continues to find new ways to connect the industry and facilitate its sustainable growth. time New Cannabis Ventureshe is responsible for content development and strategic alliances. Before turning his attention to the cannabis industry in early 2013, Alan, who began his career on Wall Street in 1986, worked as an independent research analyst with more than two decades of research and portfolio management experience. A prolific writer, with over 650 articles published since 2007 Looking for Alphawhere he has 70,000 followers, Alan is a frequent speaker at industry conferences and frequent source Media including the NY Times, Wall Street Journal, Fox Business and Bloomberg TV. Contact Alan. Twitter: |: Facebook |: LinkedIn: |: El

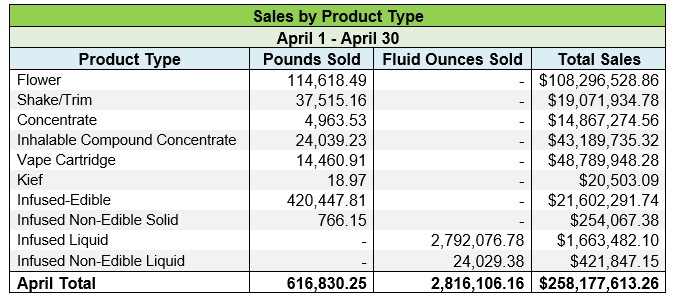

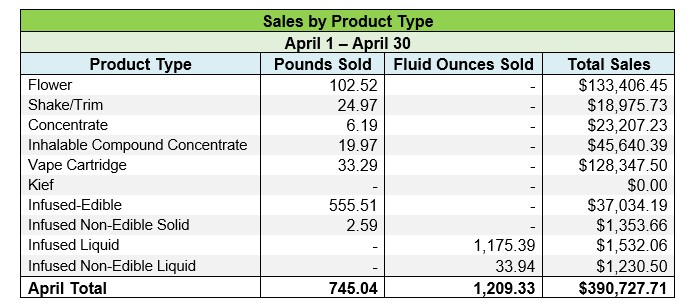

Michigan April hemp sale decreased compared to a year ago, as they increased sequentially by 1.2%. At $258.6 million, sales decreased by 4.3 percent compared to last year.

Michigan’s cannabis regulatory agency breaks down sales by medical and adult use, with medical sales down 24.1% year-over-year to $0.4 million, down 5.6% sequentially, and adult-use sales down 4.3% year-over-year to $255.5 million, despite a one-day increase of 1.2% in March.

The state breaks down sales by category and provides pricing details by category for both medical and adult;

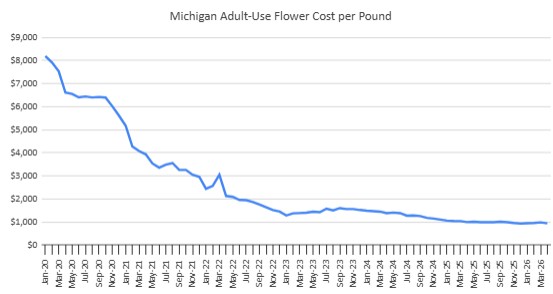

As supply continues to expand, adult flower prices have fallen sharply, although the decline is slowing. April’s average price of $945 per pound fell 4.2% sequentially to just above December’s record low and down 5.1% from a year ago.

Michigan hemp sales are expected to grow 82.1% to $1.79 billion in 2021, 27.9% to $2.29 billion in 2022, and 33.3% to $3.06 billion in 2023. billion In 2026, Michigan cannabis sales decreased by 5.9%.

Based in Houston, Alan leverages his experience as an online community founder 420 Investorthe first and still the largest due diligence platform focused on publicly traded stocks in the cannabis industry. With his extensive network in the cannabis community, Alan continues to find new ways to connect the industry and facilitate its sustainable growth. time New Cannabis Ventureshe is responsible for content development and strategic alliances. Before turning his attention to the cannabis industry in early 2013, Alan, who began his career on Wall Street in 1986, worked as an independent research analyst with more than two decades of research and portfolio management experience. A prolific writer, with over 650 articles published since 2007 Looking for Alphawhere he has 70,000 followers, Alan is a frequent speaker at industry conferences and frequent source Media including the NY Times, Wall Street Journal, Fox Business and Bloomberg TV. Contact Alan. Twitter: |: Facebook |: LinkedIn: |: El

You are reading this week’s edition of New Cannabis Ventures, a weekly magazine we have published since October 2015. The newsletter includes unique insight to help our readers stay ahead of the curve, as well as links to the most important news of the week. We no longer email them like we used to, but post this and all newsletters on our website here.

friends,

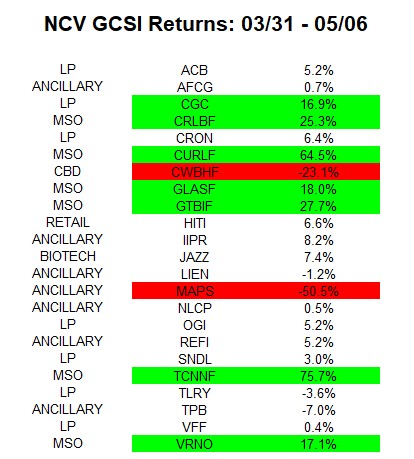

The New Cannabis Ventures Global Cannabis Stock Index edged up slightly in May, rising 1.1% to 5.76. Compared to the previous year, it decreased by 12.6%. The index, recalculated as of the end of the first quarter, is up 9.9% so far in the second quarter, lagging the S&P 500’s 12.8% gain. Here are the earnings of the 23 names currently in the index (SMG was dropped in late April after the sale of Hawthorne Gardening):

MSOs are very much higher as the rally approaches the discussion of the big transformation announcements on 4/22 and beyond. There are currently six MSOs and two of them have been promoted. The rest rose, and the average of the six was 38.1%. The AdvisorShares Pure US Cannabis ETF ( MSOS ) has rallied 48.5% since the end of March and is now up 11.7% year-to-date in 2026. Both GCSI names have fallen sharply, and the index has a total of seven double-digit gains in Q2, with six MSOs and Canopy holding investments. 14 of the 23 names returned less than GCSI.

As readers are probably aware, the US reclassified medical cannabis from Schedule I to Schedule III on 4/23, and that will go away. 280E tax for some of the businesses of cannabis companies. The Department of Justice will hold a hearing in late June to determine possible rezoning for adult use. If it passes, all 280E taxation will end, which is a good thing for cannabis companies and their investors, as well as the subsidiaries that serve them. It is not yet known what the outcome will be, and it is not yet known how past 280E taxes that have not been paid but are carried as liabilities (and not debt) will be handled. Also, there is no conclusion yet on SECURITY banking or the possibility of a raise.

NCV has stopped publishing news, although we continue to update the financial calendar as well as the earnings rankings. After more than 10 years with NCV and more than a dozen years with 420 Investor, I am in the process of moving on. I’ve appreciated sharing the news and my views here, and I want to wish everyone the best. Hopefully, the 280E taxation will end and the bear market that started in early 2021 for the hemp sector will come to an end.

Sincerely,

Alan:

This week’s newsletter is sponsored by the Paul E. Saperstein Co.

Massachusetts hemp production equipment for sale

On May 12, Middlesex Integrative Medicine, Inc.’s equipment is being auctioned online in Leominster, Massachusetts at 10:00 a.m. ET. All applications must be submitted online. Learn more Of the secured party’s sale of all assets of this cultivation equipment.

Interested parties may contact Paul Cotto at 617-227-6553 or email pcotto@pesco.com:.

New Cannabis Ventures publishes curated articles as well as exclusive news. Here is what we have published in the last 2 weeks.

Exclusives

Sales of Canadian hemp continued in February

View: Public Hemp Company Revenue and Earnings Trackingwhich ranks the highest-earning hemp stocks.

Stay on top of the most important communications from public companies by watching what’s coming cannabis investor calendar.

Based in Houston, Alan leverages his experience as an online community founder 420 Investorthe first and still the largest due diligence platform focused on publicly traded stocks in the cannabis industry. With his extensive network in the cannabis community, Alan continues to find new ways to connect the industry and facilitate its sustainable growth. time New Cannabis Ventureshe is responsible for content development and strategic alliances. Before turning his attention to the cannabis industry in early 2013, Alan, who began his career on Wall Street in 1986, worked as an independent research analyst with more than two decades of research and portfolio management experience. A prolific writer, with over 650 articles published since 2007 Looking for Alphawhere he has 70,000 followers, Alan is a frequent speaker at industry conferences and frequent source Media including the NY Times, Wall Street Journal, Fox Business and Bloomberg TV. Contact Alan. Twitter: |: Facebook |: LinkedIn: |: El

Weed Talk News Special Report Aaron Smith Executive Director NCIA 1 v 1 with PCM Founder Jimmy Young

LAGANGA ESTRANJA | BUNTZ

Marijuana Retail Report

We don’t really deal with a lot of mites because of our IPM program

California Bill To Legalize Marijuana Dispensary Drive-Thru Windows Advances In Senate After Clearing Full Assembly

Trulieve Set to List on NYSE

ABC Blocks of Weed Talk News with Alaina Pinto. Coast to coast cannabis news coverage

WHAT ARE THE LATEST ADVANCES IN CANNABIS RESEARCH? | GEORGE HODGIN

Marijuana Retail Report

Concert Series Specials launched for state medical cannabis patients

“Our system can manage equipment across 10,000+ m² using just a few wires”

Florida Workshop to Discuss What Constitutes a ‘Cartoon’ in Hemp Packaging

Mazar-i-Sharif Hash Wednesday

Afghan Black Hash Wednesday

Weak Michigan Cannabis Sales Again in July – New Cannabis Ventures

From Finance to Wellness: Brad Zerman’s Impactful Pivot

Re-release of the full show of Cannabis Coast to Coast news. Republican Texas DA Fires Up vs. laws;

DEA’s Cole Reverses His “priorities” ; Prohibitionists Dig In; Dead & Co Celebrates 60 years in SF

Your Cannabis Business: Consistent Filings Are Critical

Texas DA Fires Up for Change! Mass. Sheriff arrested on Extortion charges; GOP vs Industry in state

-

Cannabis News10 months ago

Cannabis News10 months ago“Our system can manage equipment across 10,000+ m² using just a few wires”

-

Florida10 months ago

Florida10 months agoFlorida Workshop to Discuss What Constitutes a ‘Cartoon’ in Hemp Packaging

-

Video8 months ago

Video8 months agoMazar-i-Sharif Hash Wednesday

-

Video8 months ago

Video8 months agoAfghan Black Hash Wednesday

-

aawh10 months ago

aawh10 months agoWeak Michigan Cannabis Sales Again in July – New Cannabis Ventures

-

Video10 months ago

Video10 months agoFrom Finance to Wellness: Brad Zerman’s Impactful Pivot

-

Video10 months ago

Video10 months agoRe-release of the full show of Cannabis Coast to Coast news. Republican Texas DA Fires Up vs. laws;

-

Video10 months ago

Video10 months agoDEA’s Cole Reverses His “priorities” ; Prohibitionists Dig In; Dead & Co Celebrates 60 years in SF