Cannabis News

Supply and Demand Curves Starting to Become Efficient in California as Thousands of Cannabis Growers Call It Quits

The struggles that California’s cannabis companies have been grappling with have been no secret. Still, it wasn’t until this year that a noticeable decline in the legal marijuana market started to unfold. According to permit statistics from the California Department of Cannabis Control, the market has shrunk by approximately 29%.

As of October 24, the state had only 9,900 active business licenses, marking a 28.5% decrease since July 2022, when there were 12,719 active provisional and annual cannabis business licenses, as reported by the DCC.

What Does the Stat Says

During the COVID-19 pandemic, the state’s marijuana market exhibited robust growth, benefiting from stay-at-home orders and emergency financial assistance. In July 2021, the California Department of Cannabis Control (DCC) reported 11,335 active business licenses. Over the subsequent year, the market expanded by more than 12%.

The most significant changes were observed in the cultivation sector. In July 2021, there were 7,897 active marijuana cultivation permits, which increased to 8,453 within a year but subsequently dropped to 5,727 as of October 24 this year.

The manufacturing and distribution sectors also experienced substantial fluctuations. In July 2021, there were 877 cannabis manufacturers, and this number grew to 911 over the next 12 months before decreasing to 768 this month. Among distributors, there were 1,168 in July 2021, 1,448 in July 2022, and only 1,297 this month.

However, not all sectors have experienced a similar level of decline. The retail, delivery, and microbusiness permit categories have steadily grown over the past two years. Nonetheless, industry insiders suggest that the opening of new stores has been counterbalancing the closure of many well-established shops in oversaturated cities.

Recent examples of closures include Liberty Cannabis-owned shops in both San Francisco and Los Angeles, as highlighted by marijuana consultant Hirsh Jain of Ananda Strategy. Additionally, several multistate operators, such as Florida-based Trulieve Cannabis Corp. and Arizona-based 4Front Ventures Corp., have exited the California market. This is due to the challenging market conditions, a move echoed by numerous smaller companies and brands.

Despite the challenging trends, retail storefront permits showed remarkable resilience. In July 2021, they numbered 774, then surged to 1,056 a year later, and as of this month, they have reached 1,229, according to the DCC.

Delivery licenses, on the other hand, were at 322 in July 2021, increased to 475 in July 2022, and have since stabilized at around 477. Microbusiness permits, which often include retail operations, were at 297 in July 2021, grew to 376 within a year, and currently stand at 402.

Struggles To Pay Tax

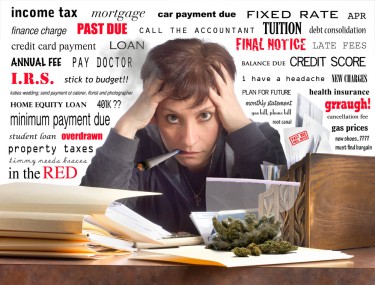

The California cannabis industry is teetering on the edge of what some are calling an “extinction event” as cannabis shops struggle to stay afloat, grappling with missed tax payments and drowning in millions of dollars of debt.

Debt troubles have haunted the industry for years, with a 2022 report estimating that the collective debt burden exceeded $600 million. Nevertheless, a recent alteration in tax regulations, which took effect this year, has prompted stakeholders to worry that the burgeoning debt crisis could potentially culminate in a severe disaster.

In reaction to these apprehensions, a San Francisco lawmaker proposed a bill in the state legislature to enforce stricter measures on cannabis businesses that cannot fulfill their debt responsibilities.

A significant shift in state law has shifted the responsibility for paying cannabis excise taxes from distributors to retailers. Historically, retailers have faced the most challenges in meeting their financial obligations, and recent state tax data obtained by SFGATE indicates that many shops lack the necessary funds to cover their state excise taxes.

More than 13% of California’s retailers, equivalent to 265 cannabis dispensaries, did not remit any tax payments, as reported by the California Department of Tax and Fee Administration. These businesses are now confronting a 50% penalty on their outstanding tax obligations, a financial blow that could prove fatal for many shops.

Furthermore, the number of affected shops could potentially increase. The state agency has revealed that it is still handling 581 tax returns, which may include retailers that failed to meet their payment obligations.

According to Michelle Mabugat, a cannabis attorney at the Greenberg Glusker firm in Los Angeles, the debt-related challenges are likely to force the closure of numerous shops in the state. She remarked that there’s been a mounting debt bubble over the past few years, reaching a breaking point. She anticipates many retailers going out of business this year, much like we witnessed with cultivators last year.”

Ali Jamalian, the owner of Sunset Connect, a cannabis manufacturer based in San Francisco, has observed pot shops with outstanding bills exceeding $500,000. He foresees the new tax structure triggering what he terms an “extinction event” for cannabis retailers in the state.

The persistent issue of debt has plagued the entire cannabis supply chain. Farmers have voiced concerns about not receiving payment for significant amounts of their products. Distributors have raised issues about non-payment by retailers and have resorted to blacklisting certain shops.

Furthermore, even the federal government has encountered payment issues. An analysis conducted last autumn by Green Market Report revealed that the ten largest cannabis companies in the country collectively owed over $500 million in unpaid taxes.

These financially strained retailers are now facing the possibility of closure due to the recent alteration in the state’s tax payment process. The state’s decision to transfer the responsibility for tax payments from distributors to retailers not only eliminated a source of financing (as retailers had been using excise tax collections to fund their operations) but also imposed a substantial penalty on cash-strapped retailers.

Conclusion

The California cannabis industry has faced significant challenges, with a 29% decline in active business licenses since July 2022. Despite growth during the COVID-19 pandemic, the cultivation sector saw fluctuations, and some multistate operators left the market due to its difficulty. However, the retail, delivery, and microbusiness sectors continued to grow, partly thanks to new store openings.

The shift in tax legislation, placing a heavier burden on retailers for paying excise taxes, has further strained the industry, with many retailers failing to meet their obligations. The industry’s future hinges on its ability to adapt to changing market conditions and proposed legislative solutions.

CALI WEED COMPANIES CAN’T PAY THEIR BILLS, READ ON…

Cannabis and the Authoritarian State

Cannabis has been legal for longer than it has been illegal. Let that sink in for a minute. For thousands of years, humans cultivated and consumed cannabis freely across civilizations and continents. It wasn’t until the early 1900s that we witnessed a massive push to drive hemp and cannabis into the black market, primarily due to industrial competition from petrochemicals, pharmaceuticals, and other industrial applications.

What makes cannabis so threatening to powerful interests? For starters, hemp and cannabis are highly versatile crops with over 50,000 different uses, from medicine to textiles to fuel. Even more remarkable is how this plant is hardwired to work with the human body through our endocannabinoid system—a biological network we didn’t even discover until the 1990s.

Perhaps most threatening of all is that cannabis is insanely easy to grow. This means that if the plant helps you with a particular physical ailment, you have the ability to grow your own medicine indefinitely. No insurance premiums, no wait lists, no pharmaceutical middlemen—just you cultivating your own healing directly from the earth.

Authoritarians do not like this, not one bit. When people can meet their own needs independently, power structures lose their grip. When citizens can think differently without permission, control systems begin to fail. So today, we’re going to look at the interesting relationship between authoritarianism and cannabis, and how this humble plant plays a key role in keeping you free.

We’ve already established the versatility of cannabis, but there’s another element that those old D.A.R.E. PSAs inadvertently reveal about what authoritarians think about cannabis. I’m talking, of course, about “behavior.” You see, in an authoritarian system, you and I are but cogs in the machine. We’re the expendables who should be proud to work ourselves to death for our “fearless leaders.”

This is precisely why certain ideas, philosophies, religions, movements, books, and substances are typically banned in authoritarian regimes. Take North Korea as an example: everything from the type of television citizens watch to the music they hear is a tightly spun spell designed to keep the populace in check. While they don’t have explicit laws against hemp (they actually grow it industrially), smoking psychoactive cannabis is strictly forbidden.

Contrast this with places like Malaysia, where you can get up to 5 years for possessing just 20 grams of cannabis, and even face the death penalty depending on the situation. These authoritarians don’t play around when it comes to cannabis because they know it affects the behavior of their populace in ways they can’t control.

The question becomes: what behavior do they fear so much that cannabis produces within the individual?

The answer is a critical mind. People who consume cannabis often begin to question their own belief systems. Most regular users undergo some transformation in their values and perspectives. Cannabis has a unique way of helping people see beyond cultural programming and think outside established paradigms. It can make the familiar strange and the strange familiar—a psychological state that’s antithetical to authoritarian control.

This independent thinking runs counter to the narrative of authoritarians who wish to maintain a tight grip on social consciousness. If even 10% of a population begins to pivot in their behavior within a regime, it can have massive ripple effects. Just look at cannabis in the US—it went from being demonized to being embraced by the majority in less than 80 years, despite massive propaganda efforts.

For authoritarians, psychoactive cannabis isn’t primarily a threat to public health and wellbeing—it’s a threat to the health and wellbeing of authoritarianism itself. When people start thinking differently, they start living differently. When they start living differently, they start demanding different. And that’s the beginning of the end for any system built on unquestioning obedience.

Beyond the threat to thought control, there’s another reason why drugs in general remain illegal: the state can use prohibition as a weapon against the populace. This isn’t conspiracy theory—it’s documented history.

Take Nixon’s war on drugs. His domestic policy chief, John Ehrlichman, later admitted: “We knew we couldn’t make it illegal to be either against the war or black, but by getting the public to associate the hippies with marijuana and blacks with heroin, and then criminalizing both heavily, we could disrupt those communities.” Nixon essentially placed cannabis on the Controlled Substances Act because he needed an excuse to shut down anti-war protests and target Black communities.

Since hippies and anti-war protesters were smoking “freedom grass,” making it illegal would circumvent their freedom of speech and freedom of assembly, and more importantly—turn free citizens into state property. It’s a win-win if you’re an authoritarian looking to silence dissent.

Then there’s the whole “boogeyman” complex that prohibition creates. We’re told “drug dealers” are roaming the streets preying on innocents, giving them “marihuanas” so they can do vile things. What the government conveniently leaves out is how the banks these “dealers” use to launder their money remain untouched. They don’t mention the shadier dealings of law enforcement either—like running guns into Mexico (eventually leading to the death of one of their own), or spraying poison on crops, killing and hospitalizing people because, you know…”Drugs are bad!”

Authoritarians cannot let go of the value that keeping the most widely used illicit substance in the world illegal provides them. This explains why the US hasn’t federally legalized cannabis despite nearly 80% of Americans supporting some form of legalization. It’s not because they don’t have enough research or that they’re genuinely concerned about public health—it’s because prohibition gives them all the privileges of violating constitutional rights while siphoning money into their coffers.

Drug prohibition creates a perpetual enemy that can never be defeated, allowing endless justification for surveillance, militarized police, asset forfeiture, and expansion of state power. What authoritarian could resist such a convenient tool?

Cannabis is a plant. You can’t make nature illegal—it’s counter to the human experience. When governments attempt to criminalize a naturally occurring organism that humans have cultivated and used for thousands of years, they reveal the absurdity of their position and the limits of their authority.

While the United States isn’t a full-on authoritarian state (yet), the truth is that many authoritarian elements have played out over the years. You only need to look as far as the war on drugs to see how the state utilizes prohibition as a weapon to their advantage. From no-knock raids to civil asset forfeiture to mass incarceration, drug laws have erected a parallel legal system where constitutional protections often don’t apply.

The fundamental truth is that cannabis is not only versatile and medicinal, it gives you back your autonomy in multiple ways. It helps you think for yourself. It allows you to grow your own medicine. It connects you with a plant that humans have used ceremonially, medicinally, and industrially throughout our history. And this autonomy is something authoritarians cannot stand—free individuals who know how to think beyond the narratives they’re fed.

Cannabis doesn’t just get you high—it offers a perspective from which the absurdities of prohibition become glaringly obvious. Perhaps this is why, as state after state legalizes, we’re witnessing the slow but steady unraveling of one of the most enduring authoritarian policies in American history.

So if you count yourself among those who value freedom of thought and bodily autonomy, who believe that nature doesn’t require government permission, and who understand that true liberty includes the right to explore your own consciousness—well, maybe it’s time to toke one up for freedom!

LEGALIZING CANNABIS IS NOT ENOUGH, READ ON..

Don’t Fertilize Your Weed with Bat Poop

Fertilization is a critical step for growing healthy marijuana plants.

They help provide essential nutrients for marijuana in various stages of growth, while promoting plant growth. There are dozens of different fertilizers to choose from in the market; growers can choose based on budget, nutrients needed, location, season, and much more. But not all fertilizers are made equally – of course, some are of better quality than others.

That said, there are some rather unusual fertilizers that can be used on plants. These may include, but are not limited to: coffee, milk, grass clippings, banana peels, fish tank water, potato water, and even urine! Yes, it does sound strange, but to gardening enthusiasts, there is nutritional value to be found in each of these things, which can make them suitable fertilizers depending on the circumstances.

For example, grass clippings make excellent mulch and can provide potassium, nitrogen, and phosphorus. Urine is a potent source of nitrogen as well as phosphorus. Banana peels are rich in calcium, which is excellent for promoting root growth while helping supply oxygen to the soil.

But what about bat poop? Also known as guano, bat poop has been said to work as a plant fertilizer because it’s rich in nitrogen, potassium, phosphorus, and other nutrients. Unfortunately, using bat poop as a plant fertilizer can also be dangerous. So if you don’t really know what you are doing, bat poop as a fertilizer can be extremely risky.

Bat Poop Fertilizer Kills 2 NY Men

On December 2024, news of two men hailing from Rochester, New York, dying went viral.

The cause of death was dangerous fungus, in the bat poop that they were using to fertilize their marijuana plants. Both men grew their own marijuana plants for medical consumption, but unfortunately developed histoplasmosis after breathing toxic fungal spores from the guano.

One of the men was aged 59 years old; he bought bat poop online to use as fertilizer for his plants. Meanwhile, the other was a 64-year-old male who found guano in his attic, then decided to use it to fertilize his cannabis plants. They both developed similar symptoms, including chronic coughs, fever, severe weight loss, and respiratory failure. The case was also discussed in the Open Forum Infectious Diseases medical journal.

Is there a safe way to use bat poop as fertilizer? If you ask me, I truly can’t understand why one would use guano as fertilizer when there are so many other proven safe alternatives out there that are simply not as risky. According to the University of Washington, one must always wear a dust mask each time you open a bag containing soil amendments. That’s because a mask will greatly decrease the chances of breathing in fungal spores, which could be potentially dangerous. They also go on to explain that yes, guano is indeed used as fertilizer for its valuable nitrogen content but it still isn’t without its own risks, particularly of developing Histoplasma – the same condition that killed the two men.

Make Your Own Safe Fertilizers At Home

There are many other safe, affordable – and even free – fertilizers you can feed your marijuana plants with. It doesn’t have to cost a fortune nor does it have to be risky to your health.

Check out these easy, low-cost, DIY fertilizers for weed:

-

Coffee grounds are abundant in nitrogen, which makes it perfect for the vegetative stage of marijuana plants. They are also a fantastic source of organic materials and green waste, which contain other vital nutrients. When the coffee grounds decompose, they create soil aggregates that improve soil aeration and its water retention capabilities.

Mix around 2 grams of coffee ground for every liter of soil. Measuring its pH levels is also helpful, since you want it to be between 6 to 6.5

-

Crushed eggshells are a great way to ensure no eggshells go to waste. It’s rich in calcium plus other minerals that are effective in improving overall plant structure, health, and growth. In fact, so many gardeners and farmers commonly use crushed eggshells to help boost plant growth – and it will work just as well for marijuana plants.

They’re really easy to use, too! Just mix eggshells into the soil, or steep them into water then pour into the soil for a calcium-packed feed.

-

Banana tea or water is rich in potassium and magnesium, making it perfect as a feed during the marijuana plant’s flowering stage. You can use banana peels differently: with 3 to 5 banana peels, soak it in water for 2 days. Then you can use the water on your plants, and even leave the banana peels as compost for your garden.

-

Wood ash from your fireplace or other sources is a great source of phosphorus and potassium. Simply sprinkle some wood ash over marijuana during the final flower phase. Just use 1 or 2 grams of ash for every liter of substrate. Be careful not to use too much wood ash, or it can make the soil too alkaline.

-

Animal manure, such as those from cows, rabbits, or horses, make excellent organic fertilizers. Just be sure that they’re composed properly so that you avoid introducing weed seeds, or pathogens.

These low-cost fertilizers are also natural and effective. There’s no reason for you to turn to bat poop as fertilizer, even if you’re in a bind.

Conclusion

Guano or bat poop is a poor choice of fertilizer if you don’t know what you are doing. It’s risky and potentially dangerous – just not worth it. Instead, fertilize your marijuana plants with these options mentioned.

BEST POOP FOR CANNABIS PLANTS, KEEP READING…

Edible Arrangements Leans into Intoxicating Hemp Products: A Strategic Expansion

Edible Arrangements, a brand renowned for its vibrant fruit bouquets and sweet treats, is embarking on a bold new venture into the hemp and THC-infused edibles market. Through its parent company, Edible Brands, the company has launched Edibles.com, an e-commerce platform offering a variety of hemp-based products such as THC-infused beverages, gummies, and snacks. This strategic move taps into the burgeoning demand for cannabis-related wellness products and reflects a deliberate expansion beyond traditional offerings.

Introduction to Edible Arrangements and Its New Venture

Edible Arrangements was founded in 1999 by Tariq Farid, who envisioned a unique way to gift fresh fruit arrangements that were both visually appealing and delicious. Over the years, the company has grown to become a global brand with hundreds of locations across the United States and internationally. However, the company’s latest initiative marks a significant departure from its traditional fruit-based offerings, signaling a broader strategic shift towards becoming a comprehensive food, health, and wellness company.

The New Venture: Edibles.com

Edibles.com debuted on March 20, 2025, starting operations in Texas with ambitious plans to expand rapidly across Southeastern states like Florida and Georgia. The platform is designed to cater to consumers aged 21 and older, providing low-dose THC products that comply with the 2018 Farm Bill, which legalized hemp containing less than 0.3% THC by dry weight. Select products will also be available for nationwide shipping where legally permitted, leveraging the company’s existing logistics infrastructure.

Product Lineup

The initial product lineup includes a range of THC-infused beverages, gummies, and snacks. These products are designed to appeal to both seasoned cannabis users and newcomers looking for low-dose, accessible options. The company emphasizes the importance of quality and safety, ensuring that all products undergo rigorous testing to meet high standards of purity and potency.

Strategic Alignment and Market Potential

The move into the infused edibles market aligns with Edible Brands’ vision of becoming a broader food, health, and wellness company. CEO Somia Farid Silber highlighted that the infused edibles market is a fast-growing sector with high consumer demand for safe and reliable products. The company is leveraging its extensive franchise network to deliver these items while planning to open brick-and-mortar stores under the Incredible Edibles brand.

Market Trends and Consumer Demand

The cannabis industry, particularly the segment focused on hemp and THC-infused products, has seen exponential growth in recent years. This growth is driven by increasing consumer interest in wellness and recreational products, as well as evolving legal landscapes that have opened up new markets. Edible Arrangements is positioning itself to capitalize on this trend by offering products that cater to both health-conscious consumers and those seeking unique gifting options.

Challenges and Opportunities

While this expansion offers significant growth potential, it also comes with challenges such as navigating varying state regulations and ensuring product safety and quality. The company aims to address these issues through robust infrastructure and consumer advocacy. Thomas Winstanley, a cannabis industry veteran leading Edibles.com, emphasized the company’s unique position to drive innovation in this emerging market.

Regulatory Challenges

One of the primary challenges facing Edible Arrangements is the complex regulatory environment surrounding cannabis products. Laws regarding the sale and distribution of THC-infused products vary significantly from state to state, requiring the company to adapt its operations to comply with local regulations. This includes ensuring that products meet specific THC content limits and are marketed responsibly.

Quality Control and Safety

Another critical challenge is maintaining high standards of quality and safety across all products. Edible Arrangements is investing heavily in testing and quality assurance processes to ensure that all products meet stringent safety standards. This includes partnering with reputable suppliers and implementing rigorous testing protocols to verify the potency and purity of all THC-infused items.

Consumer Education and Advocacy

As part of its strategy, Edible Arrangements is also focusing on consumer education and advocacy. The company recognizes that many consumers are new to cannabis products and may have questions about usage, dosage, and safety. To address this, Edibles.com will provide comprehensive product information, dosage guidelines, and resources for consumers to learn more about the benefits and risks associated with THC-infused products.

Marketing Strategy

Edible Arrangements plans to leverage its existing brand recognition and customer loyalty to promote its new line of hemp-based products. The company will utilize social media, email marketing, and targeted advertising to reach its target audience. Additionally, partnerships with influencers and cannabis industry experts will help build credibility and drive awareness about the brand’s entry into this new market.

Future Expansion Plans

In the coming months, Edible Arrangements plans to expand its operations beyond Texas, targeting key markets in the Southeast. The company is also exploring opportunities to open physical stores under the Incredible Edibles brand, which will offer a curated selection of THC-infused products alongside traditional Edible Arrangements items.

Incredible Edibles Stores

The Incredible Edibles stores will serve as a unique retail experience, combining the company’s traditional fruit arrangements with its new line of hemp-based products. This format will allow customers to explore and purchase THC-infused items in a welcoming and educational environment. The stores will also host workshops and events focused on cannabis education and wellness, further enhancing the brand’s position as a leader in this emerging market.

Conclusion

Edible Arrangements’ foray into the hemp and THC-infused edibles market marks a significant strategic shift for the company. By leveraging its brand recognition and logistical capabilities, Edible Arrangements is poised to become a major player in this rapidly growing sector. While challenges exist, the company’s commitment to quality, safety, and consumer education positions it well for success in this new venture.

As the cannabis industry continues to evolve, Edible Arrangements’ entry into this market underscores the broader trend of mainstream brands embracing cannabis-related products. This move not only expands the company’s offerings but also reflects a broader cultural shift towards greater acceptance and normalization of cannabis use.

HEMP-DERIVED THC DELIVERIES ARE HERE, READ ON…

Cannabis Can Help A Sore Throat

Cannabis and the Authoritarian State

As cannabis consumer tastes evolve, industry must look beyond potency

Article: Early 2025 Empire State Psychedelic Policy Roundup

White House Finally Comments On Marijuana Industry

Stop Using Bat Poop to Fertilize Your Weed Plants Immediately, Here is Why…

The History Behind April Fool’s Day

Star signs and cannabis strains: April 2025 horoscopes

Does Comfort Food Actually Help

Connect to cannabis history with three legacy strains from Paradise Seeds

Distressed Cannabis Business Takeaways – Canna Law Blog™

United States: Alex Malyshev And Melinda Fellner Discuss The Intersection Of Tax And Cannabis In New Video Series – Part VI: Licensing (Video)

What you Need to Know

Drug Testing for Marijuana – The Joint Blog

NCIA Write About Their Equity Scholarship Program

It has been a wild news week – here’s how CBD and weed can help you relax

Cannabis, alcohol firm SNDL loses CA$372.4 million in 2022

A new April 20 cannabis contest includes a $40,000 purse

Your Go-To Source for Cannabis Logos and Designs

UArizona launches online cannabis compliance online course

-

Cannabis News2 years ago

Cannabis News2 years agoDistressed Cannabis Business Takeaways – Canna Law Blog™

-

One-Hit Wonders2 years ago

One-Hit Wonders2 years agoUnited States: Alex Malyshev And Melinda Fellner Discuss The Intersection Of Tax And Cannabis In New Video Series – Part VI: Licensing (Video)

-

Cannabis 1012 years ago

Cannabis 1012 years agoWhat you Need to Know

-

drug testing1 year ago

drug testing1 year agoDrug Testing for Marijuana – The Joint Blog

-

Education2 years ago

Education2 years agoNCIA Write About Their Equity Scholarship Program

-

Cannabis2 years ago

Cannabis2 years agoIt has been a wild news week – here’s how CBD and weed can help you relax

-

Marijuana Business Daily2 years ago

Marijuana Business Daily2 years agoCannabis, alcohol firm SNDL loses CA$372.4 million in 2022

-

California2 years ago

California2 years agoA new April 20 cannabis contest includes a $40,000 purse