Canadian Cannabis News

Tilray Brands Reports Q2 Cannabis Revenue Grew 5% – New Cannabis Ventures

Tilray Brands Delivers Record Q2 FY2026 Net Income of $218 Million, Moves to Net Cash Position and Reaffirms Full-Year Adjusted EBITDA Guidance.

- International Medical Cannabis Revenue Increases 36%; Cannabis income by Canadian adults increased by 6%

- Tilray Pharma achieves record quarterly revenue

- US Federal Cannabis Reregulation Expected to Open New Market Opportunity for Tilray’s Medical Expansion in the US

- Strong financial position with $292 million in cash and marketable securities¹ and ~$30 million in net cash

NEW YORK and LONDON and LEAMINGTON, Ontario, Jan. 08, 2026 (GLOBE NEWSWIRE) — Tilray Brands, Inc. (“Tilray,” “our,” “we” or the “Company”) (Nasdaq: TLRY; TSX: TLRY), a global lifestyle and consumer packaged goods company, a leader in the cannabis, beverage and health industries, today reported financial results for its second fiscal quarter ended November 30, 2025.

Irwin D. Simon, Chairman and Chief Executive Officer, commented: “We delivered another record quarter with net revenue of $218 million driven by orderly execution across our diversified portfolio spanning the cannabis, beverage, health and distribution industries. Our business model supports our scalability, market value creation, adaptability as well as long-term performance. Strengthening our core operations The quarter ended with a strong balance sheet and strong liquidity, underscoring our prudent financial management and giving us the flexibility to make selective investments in strategic growth initiatives.

Mr. Simon continued. “We believe federal realignment will mark an important step forward for medical cannabis in the United States, paving the way for more research, broader physician involvement, and better patient access. Tilray has invested over the years in developing the infrastructure, expertise and discipline necessary to operate successfully in the highly regulated medical markets. With a key role in building a responsible, research-oriented national medical cannabis industry with the team and platform already in place with Tilray Medical US, we intend to leverage the infrastructure, expertise and knowledge developed with Tilray Medical’s expected $150 million medical cannabis business and our new $300 million Tilray Pharma medical distribution platform. trials and partnerships for product development”.

_________________________

¹Cash and marketable securities and net (borrowed) cash are non-GAAP financial measures. See “Use of Non-GAAP Measures” below for further discussion of these non-GAAP measures and a reconciliation of this non-GAAP measure to our most comparable GAAP measure.

Financial milestones

All comparisons with the previous year period

- Net income rose 3% in the second quarter to $217.5 million from $211.0 million.

- Gross profit in the second quarter was 57.5 million dollars, against 61.2 million dollars.

- Gross margin was 26% in the second quarter, up from 29%.

- Cannabis net revenue increased 3% to $67.5 million in the second quarter, compared to $65.7 million, driven by 36% growth in international cannabis and 6% growth in Canadian adult cannabis, offset by a lower presence of Canadian bulk cannabis in anticipation of deployment in international markets.

- Cannabis’ gross profit rose to $26.1 million in the second quarter, up from $23.2 million.

- In the second quarter, hemp gross margin increased to 39% from 35%.

- Beverage net revenue in the second quarter was $50.1 million, compared to $63.1 million.

- Beverages gross profit in the second quarter was $15.7 million, compared to $25.2 million.

- Beverages gross margin was 31% in the second quarter, up from 40%.

- Wellness net income was flat at $14.6 million in the second quarter.

- Wellness’s gross profit rose to $4.6 million in the second quarter from $4.5 million.

- Health’s gross margin increased to 32% from 31% in the second quarter.

- Net distribution income, which includes Tilray Pharma, increased to our highest revenue quarter ever to $85.3 million in the second quarter, up from $67.6 million in the second quarter.

- The distribution’s gross profit increased to $11.0 million in the second quarter, compared to $8.4 million.

- In the second quarter, gross distribution margin increased to 13% from 12%.

- Second-quarter net loss improved to $43.5 million from $41.8 million, compared to a net loss of $85.3 million, and second-quarter net loss per share improved to $0 ($0.41) from $0.99.

- Adjusted net loss² and adjusted net loss per share2 improved to $(2.0) million and $(0.02) in the second quarter, compared to $(0.02) and adjusted net loss of $(2.2) million and $(0.03). Excluding non-cash income tax charges, adjusted net income and adjusted net income per share would have been $1.6 million and $0.01.

- Adjusted EBITDA³ was $8.4 million in the second quarter, compared to $9.0 million.

Cash flows. Cash used in operations improved from $32.2 million to $8.5 million from $40.7 million.

Balance update. In the second quarter, we increased our cash and marketable securities balance to $291.6 million, providing flexibility for strategic opportunities. In addition, we reduced our total outstanding debt by $4.2 million, further strengthening the balance sheet.

Net (debit) Cash position. Our Q1 net debt position of $3.8 million improved sequentially by $31.2 million to a total net cash position of $27.4 million.

Adjusted EBITDA guidance for fiscal 2026 restated to $62 million – $72 million

Published by NCV Newswire

New Cannabis Ventures’ NCV Newswire aims to gather high-quality content and information about leading cannabis companies to help our readers filter through the noise and stay on top of the most important cannabis business news. The NCV Newswire is edited by an editor and is not, however, automated. Got a secret news tip? Get in touch.

Tilray Brands Delivers Record Quarter 2026 Financial Results; Net income increased to $207 million, an 11% organic increase, and gross profit increased to $55 million, a 6% year-over-year increase.

- International Hemp Accelerates With 73% Net Revenue Growth and 100% YoY Growth in Cannabis Flower Sales

- Canadian adult-use and medical cannabis net revenue up 8% year-over-year; Tilray maintains the No. 1 cannabis leadership position in Canada by revenue

- BrewDog Acquisition¹ for ~£40m cash positions Tilray as a global beverage leader with multi-regional expansion across Europe, the Middle East, Australia, Asia-Pacific and the US

- Strong balance sheet supports growth with $265 million in cash and marketable securities² and ~$3.5 million in net cash

NEW YORK and LONDON and LEAMINGTON, Ontario, April 01, 2026 (GLOBE NEWSWIRE) — Tilray Brands, Inc. (“Tilray,” “our,” “we” or the “Company”) (Nasdaq: TLRY; TSX: TLRY), a global consumer packaged goods company and leader in the cannabis, beverage and health industries, today reported financial results for its third fiscal quarter ended February 28, 2026. revenue and the continued successful execution of its global expansion strategy. All financial information in this press release is presented in US dollars unless otherwise indicated.

“Our third quarter results demonstrated the strength of our global strategy, delivering our strongest quarter of net income and gross profit to date. Our international hemp business delivered its best quarterly net income in company history, reflecting more than 70% year-over-year growth in our global strategy. markets We see our strategy working by driving growth through scale, product innovation and strong distribution.

Mr. Simon continued. “With the acquisition of leading British craft beer brand BrewDog and our recently announced partnership with Carlsberg from 2027, we are accelerating the creation of a globally scalable beverage platform. These initiatives expand our infrastructure, strengthen our brand portfolio and expand our position in key distribution opportunities in Europe, expand our position in key distribution opportunities in Europe. Backed by our diverse platform in the Middle East, Australasia and Asia-Pacific across cannabis, beverages, pharmaceutical distribution and health, we are well-versed in industry adversaries while capitalizing on emerging opportunities driven by global consumer trends and regulatory changes.

_________________________

1 The BrewDog acquisition is not reflected in the Company’s third quarter results or balance sheet as the transaction was closed and completed after the end of the quarter.

2 Cash, restricted cash and marketable securities is a non-GAAP financial measure. See “Use of Non-GAAP Measures” below for further discussion of these Non-GAAP measures and a reconciliation of such Non-GAAP Measures to our most comparable GAAP measure.

Financial milestones

All comparisons with the previous year period

- Net income rose 11% to a record $206.7 million in the third quarter, up from $185.8 million.

Third-quarter gross profit rose 6% to a record $55.0 million from $52.0 million.

Gross margin was 27% in the third quarter, up from 28%.

Cannabis net revenue increased 19% to $64.8 million in the third quarter, compared to $54.3 million, driven by a 73% increase in international cannabis revenue and an 8% increase in Canadian adult use and medical cannabis net revenue.

Cannabis’ gross profit rose 18% to $26.0 million in the third quarter from $22.0 million.

Hemp gross margin was 40% in the third quarter, up from 41%.

Beverage net revenue in the third quarter was $42.6 million, compared to $55.9 million.

Beverages gross profit in the third quarter was $13.6 million, compared to $19.9 million.

Beverages gross margin was 32% in the third quarter, up from 36%.

Health net income rose 16% to $16.4 million in the third quarter from $14.1 million.

Health’s gross profit rose 19% to $5.4 million in the third quarter from $4.5 million.

Health’s gross margin increased to 33% from 32% in the third quarter.

Distribution net income, which includes Tilray Pharma, rose to a record third-quarter net income of $83.0 million, up from $61.5 million.

The distribution’s gross profit rose to $10.0 million in the third quarter from $5.6 million.

Gross distribution margin increased to 12% from 9% in the third quarter.

Net loss improved 97% in the third quarter to $25.2 million on a net loss of $793.5 million, and net loss per share improved to $0.24 in the third quarter (from $8.69).

Adjusted net income (loss)³ and adjusted net income per share³ improved to $2.4 million and $0.02 in the third quarter, compared to an adjusted net loss of $2.9 million and ($0.03).

Adjusted cash operating income4 improved to $4.0 million in the third quarter, compared to a cash operating loss of $3.1 million.

Adjusted EBITDA⁵ increased 19% to $10.7 million in the third quarter from $9.0 million.

_________________________

3 Adjusted net income (loss) and adjusted net income (loss) per share are non-GAAP financial measures. See “Use of Non-GAAP Measures” below for a discussion of these Non-GAAP measures and a reconciliation of this Non-GAAP measure to our most comparable GAAP measure.

4 Adjusted cash operating income (loss) is a non-GAAP financial measure. See “Use of Non-GAAP Measures” below for a discussion of these Non-GAAP measures and a reconciliation of this Non-GAAP measure to our most comparable GAAP measure.

5 Adjusted EBITDA is a non-GAAP financial measure. See “Use of Non-GAAP Measures” below for a discussion of these Non-GAAP measures and a reconciliation of this Non-GAAP measure to our most comparable GAAP measure.

Balance update: our balance sheet remains strong with secured cash, restricted cash and marketable securities balance of $264.8 million at the end of the third quarter, providing flexibility for strategic opportunities and investments. We also reduced our total debt outstanding by $4.2 million in the quarter, highlighting our improved debt position.

Net (debt) cash position. Our net cash position of $3.5 million improved to $40.2 million compared to net debt of $36.6 million last year.

Program 420 update. In the quarter, we completed the previously announced Project 420 synergy program, delivering approximately $33 million in annualized cost savings and significantly strengthening the cost structure of our Beverages business.

FY 2026 guidance

For its fiscal year ending May 31, 2026, the Company reaffirms its guidance to achieve: adjusted EBITDA of $62 million to $72 million, representing an increase of 13% to 31% compared to fiscal 2025.

Management’s guidance for Adjusted EBITDA is provided on a non-GAAP basis and excludes stock-based compensation; change in fair value of contingent consideration. increase in purchase price accounting; impairment of intangible assets and goodwill; In addition to the temporary change in the fair value of convertible receivables; court costs; restructuring costs, transaction (revenue) costs and other non-operating income (expenses) and other non-recurring items that may occur during the Company’s 2026 fiscal year, which the Company will continue to recognize when presenting its future financial results. Given the escalation of hostilities in the Middle East, including Iran, we are monitoring various factors that may directly and indirectly affect operating expenses and, therefore, our adjusted EBITDA expectations, including energy, fuel, logistics and supply chain disruption.

The Company is unable to reconcile its expected Adjusted EBITDA with the “Fiscal Year 2026 Guidance” to net income without unreasonable effort because certain items affecting net income and other reconciliation measures are beyond the Company’s control and/or cannot be reasonably predicted at this time.

Live audio webcast

Tilray Brands will host a webcast to discuss these results today at 8:30 AM ET. Investors can tune in to the live webcast, which is available in the Events and Presentations section of Tilray’s Investor Relations website. A replay will be available and archived on the Company’s website.

About Tilray Brands

Tilray Brands, Inc. (“Tilray”) (Nasdaq: TLRY; TSX: TLRY), is a leading lifestyle and consumer packaged goods company with operations in Canada, the United States, Europe, Australia and Latin America, leading as a transformative force at the intersection of cannabis, beverages, health and entertainment. Tilray’s mission is to be a leading premium lifestyle company, home to brands and innovative products that inspire joy and create memorable experiences. Tilray’s unparalleled platform supports more than 40 brands in more than 20 countries, including comprehensive cannabis offerings, hemp-based food and craft beverages.

To learn more about how we elevate life in moments of connection, visit Tilray.com and follow @Tilray on all social platforms.

Published by NCV Newswire

New Cannabis Ventures’ NCV Newswire aims to gather high-quality content and information about leading cannabis companies to help our readers filter through the noise and stay on top of the most important cannabis business news. The NCV Newswire is edited by an editor and is not, however, automated. Got a secret news tip? Get in touch.

You are reading this week’s edition of New Cannabis Ventures, a weekly magazine we have published since October 2015. The newsletter includes unique insight to help our readers stay ahead of the curve, as well as links to the most important news of the week. We no longer email them like we used to, but post this and all newsletters on our website here.

friends,

I’m a big fan of artificial intelligence, although I have many concerns about its use. Some of the areas where I think AI can help society are healthcare diagnostics and drug discovery, finance, manufacturing, retail, logistics and technology. Workday, a publicly traded HR technology company, was discussed the ways that AI can and will affect certain industries in an article last summer.

I don’t follow WDAY closely, but the stock is down 40.8% so far in 2026, although this weakness is not unique to this stock. I have been and remain bearish on stocks, especially large-cap stocks, but I bought a tech ETF, the State Street SPDR S&P 500 Software & Services ETF, which is down 23.1% for the day. It also includes some very large companies and some that I really like. The reason these stocks have fallen so much appears to be concerns about AI, which could lead to the demise of software as a service (SaaS).

As a fan of AI, but someone who is concerned about it, I’ve been paying close attention to it even though I’m not paying for any of the services. I started using ChatGPT last year and tested it with the world I know, cannabis stocks. I was not satisfied with the answers to my questions. I recently started using Claude which I like better. I’ve never written about AI and how it can help (or hurt) people trying to pick good cannabis stocks, but I’m thinking today because I don’t think the answers are quite right.

As an analyst who has followed this industry closely for over 13 years, I know a lot. What I do know is that I don’t know everything about hemp stocks, and I certainly can’t accurately predict the future. I love that people can use the internet to do their research and it’s so much better than when I was a kid. The investment world then operated by fax, and investors had to deal with stockbrokers. AI can potentially take individuals further with their stock research.

I started writing this article before seeing this example that I will discuss. I want readers to know that this is an example of how Claude can come up with some pretty smart answers to questions. Asking good questions is the right thing for investors to do, but knowing what to do with those answers can be difficult. I believe that artificial intelligence is not there yet, and I base this on the answers to certain questions. I celebrate the improvement, but for those who think that choosing the right cannabis stock will lead to great results, I urge caution. This comment, in my opinion, goes beyond hemp stocks. Stock picking in general can be helped by artificial intelligence, but it is not harmless. Here is an example of a question I asked Claude and I think the answer is very helpful.

I am not trying to influence the price of Glass House Farms because I have literally zero influence on it. I have known Mark Codes for 50 years and love and respect him. I also think Glass House Farms CEO Kyle Kazan and his staff are doing good things.

As I’ve written here for a while, the hemp industry is facing many challenges, the biggest of which is 280E taxation. Will 280E be completed? When? Hemp stock traders and hemp stock investors need to understand that no one knows. There are many other challenges facing the hemp industry, and it goes beyond the US. Can AI answer the question of which direction hemp stocks will move in the right direction? Only if it says “up or down”.

So if you’re relying on AI to tell you when to buy cannabis stocks, or which ones to buy, I urge caution. If you’ve found something that you think gives investors a solid tool for success, please let me know. I wish readers the best with hemp stocks that remain in a bear market that is now more than five years old.

Sincerely,

Alan:

New Cannabis Ventures publishes curated articles as well as exclusive news. Here is what we have published in the last 3 weeks.

Exclusives

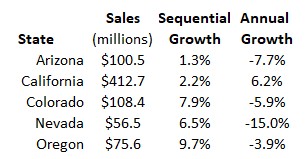

Canadian cannabis sales set to grow in 2026

Hemp companies ended 2025 in weakening financial positions

Cannabis sales plummeted in Illinois

Michigan’s cannabis sales are up slightly

Financial statements

Ascend Wellness Saw Wider Operating Loss in Q4

Verano Q4 exceeded analyst expectations

Vireo Growth is now the 7th largest MSO by revenue

Follow Alan for real-time updates X.com:. Share and discover industry news with like-minded people on the largest group of cannabis investors and entrepreneurs LinkedIn:.

View: Public Hemp Company Revenue and Earnings Trackingwhich ranks the highest-earning hemp stocks.

Stay on top of the most important communications from public companies by watching what’s coming cannabis investor calendar.

Based in Houston, Alan leverages his experience as an online community founder 420 Investorthe first and still the largest due diligence platform focused on publicly traded stocks in the cannabis industry. With his extensive network in the cannabis community, Alan continues to find new ways to connect the industry and facilitate its sustainable growth. time New Cannabis Ventureshe is responsible for content development and strategic alliances. Before turning his attention to the cannabis industry in early 2013, Alan, who began his career on Wall Street in 1986, worked as an independent research analyst with more than two decades of research and portfolio management experience. A prolific writer, with over 650 articles published since 2007 Looking for Alphawhere he has 70,000 followers, Alan is a frequent speaker at industry conferences and frequent source Media including the NY Times, Wall Street Journal, Fox Business and Bloomberg TV. Contact Alan. Twitter: |: Facebook |: LinkedIn: |: El

Grape Cake Marijuana Monday

The C Block of Cannabis Coast to Coast News-

Cannabis Lawyer Explains Hidden Risks of Rescheduling

MEGA CANNABIS BRAND BUILDER | SMOKE WALLIN [cannabis brands]

Cannabis Sales Failed to March – New Cannabis Ventures

Speakeasy Dispensary announces opening of newest Kentucky location

West Virginia Treasurer Allocates Medical Marijuana Revenue Despite Governor’s Veto

Funky Charms Marijuana Monday

Legalization update with Morgan Fox of NORML full interview Special Report w/PCM Founder Jimmy Young

Do THIS When It’s Time To Flower

“Our system can manage equipment across 10,000+ m² using just a few wires”

Florida Workshop to Discuss What Constitutes a ‘Cartoon’ in Hemp Packaging

Mazar-i-Sharif Hash Wednesday

From Finance to Wellness: Brad Zerman’s Impactful Pivot

Re-release of the full show of Cannabis Coast to Coast news. Republican Texas DA Fires Up vs. laws;

Weak Michigan Cannabis Sales Again in July – New Cannabis Ventures

DEA’s Cole Reverses His “priorities” ; Prohibitionists Dig In; Dead & Co Celebrates 60 years in SF

New Hampshire Governor Says Federal Marijuana Rescheduling Won’t Change Her Opposition To Legalization

Your Cannabis Business: Consistent Filings Are Critical

Texas DA Partakes on Tik Tok to prove a point; Boston Sheriff arrested for Extortion of $ w/ Ascend

-

Cannabis News8 months ago

Cannabis News8 months ago“Our system can manage equipment across 10,000+ m² using just a few wires”

-

Florida8 months ago

Florida8 months agoFlorida Workshop to Discuss What Constitutes a ‘Cartoon’ in Hemp Packaging

-

Video6 months ago

Video6 months agoMazar-i-Sharif Hash Wednesday

-

Video8 months ago

Video8 months agoFrom Finance to Wellness: Brad Zerman’s Impactful Pivot

-

Video8 months ago

Video8 months agoRe-release of the full show of Cannabis Coast to Coast news. Republican Texas DA Fires Up vs. laws;

-

aawh8 months ago

aawh8 months agoWeak Michigan Cannabis Sales Again in July – New Cannabis Ventures

-

Video7 months ago

Video7 months agoDEA’s Cole Reverses His “priorities” ; Prohibitionists Dig In; Dead & Co Celebrates 60 years in SF

-

Cannabis News8 months ago

Cannabis News8 months agoNew Hampshire Governor Says Federal Marijuana Rescheduling Won’t Change Her Opposition To Legalization