Cannabis News

Norway’s Saga Robotics raises funding for farm robots

Saga Robotics, Norwegian developers of the Robotic platform Torvald. The circle has closed in two trenches and moved to Thorvald from the initial market entrance to a wide-scale adoption.

The financing turn was directed by Praesidium Agri-Foodtech with the participation of existing investors, including Nysnø climate investments, Blystad, Hattaland, Melesio, Sanden and Norwegian MP Pensjon.

© saga robotics

© saga robotics

Dorn Wenninger, President of the Saga Robotics.

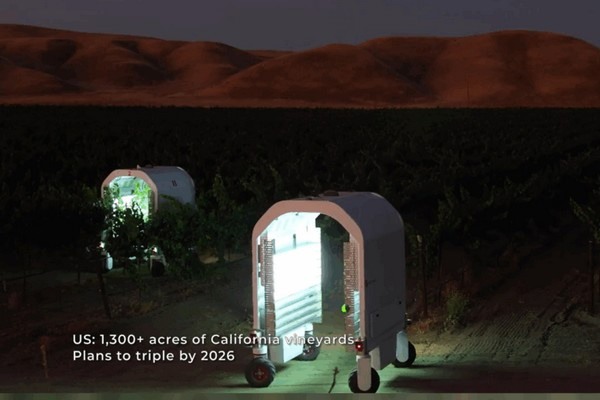

Thorvald is a modular robotic system designed for soft fruits and vineyards. Units offer tasks such as UV-C light-based diseases control, powder forecasts and crop tracking. In the 2025 season, more than 150 thorvald 3.0 units have spread.

Fresh capital will accelerate thorvald’s census. In the strawberry sector in the UK, today they are treated about 20 percent of the market, with more than a dozen, exceeding 30 percent of 2026. In the US, Saga Robotics is a triple triple triple vineyard of the current 1,300 hectares. The california program offers robotic programs, they are using to drive adoption.

Alice Laurora, President of the Praesidium Agri-Foodtech, has been completely used in 2025 acres in 2025. We are investing in the Saga robotics, proper technology, proper technology and a clear path to scale in valuable agricultural sectors. “

Founder pål Johan added. Now, we are scaling. Lifting gives us the track to accelerate adoption, improve efficiency in agriculture and reduce the chemicals in the market for two market market market in the market market in the market. “

Saga Robotics says Growth provides resources for expanding operations while locating its robotic technology within the widerage of agricultural automation.

For more information:

Global Agirevesting

Tel: +1 (978) 887 8800

Email: (Protected by email)

www.globalagingvesting.com

Well, it’s not 2026 photos, but with around 600 photos, we definitely did our best. For the past two days, the Netherlands has been the place to be for the global greenhouse industry. From Flower Trials for the horticulture sector, company visits to growers and technical suppliers, as well as dinners, get-togethers, drinks, knowledge sessions and much more. And of course with GreenTech Amsterdam.

The event brought together professionals from around the world to connect, network, share knowledge and do business.

Next week, we’ll be sharing more information on market developments, trends, what’s on display, news, business news, innovations and whatever else you can think of, but for now we’ll stick to photo reporting.

Click here for the photo report.

© Arlette Sijmonsma | MMJDaily.com

© Arlette Sijmonsma | MMJDaily.com

Cannabis News

Illinois Governor Signs Bill To Double Marijuana Possession Limit, Restrict Hemp THC Products And Reform Rules For Businesses

On May 29, 2026, global cannabis technology company CannBro was invited to the Cannabis Expo in Johannesburg to share insights on emerging cannabis-related medical applications and supply chain strategies in the cannabis markets.

At the event, CannBro highlighted its partnership with the CHEEBA Cannabis Academy to promote industry education, compliance awareness and the development of regulatory standards in emerging cannabis markets. The company highlighted the importance of establishing strong regulatory and compliance frameworks for the sustainable growth of the industry.

© CannBro

© CannBro

As a company certified with ISO 13485 and GMP, CannBro actively explores medical cannabis applications and collaborates with health organizations to discuss potential clinical research and CBD product applications.

© CannBro

© CannBro

CannBro also introduced the “Factory Pricing + Local Stock” strategy, combining manufacturing capabilities in China with warehouses located overseas, enabling efficient delivery of local inventory. The company currently operates warehouses in the United States, Canada, Germany and South Africa and has helped more than 150 customers with local stock delivery solutions that reduce costs and improve inventory turnover.

In addition, CannBro visited local cannabis cultivation facilities to learn about the evolution of the South African market and explore potential partnerships for cultivation, medical applications and product development.

© CannBro

© CannBro

Andy Zhao, CEO of CannBro, said: “As the global cannabis market matures, fulfillment and medical applications will become key drivers of sustainable growth. CannBro remains committed to advancing the industry through education, medical research and supply chain innovation.”

For more information:

CannBro Technology

Email: (email protected)

www.cannbro.com

Marijuana Retail Report

GreenTech Amsterdam 2026 in 2026 photos

Why Pharma Is Taking Cannabis Seriously

Illinois Governor Signs Bill To Double Marijuana Possession Limit, Restrict Hemp THC Products And Reform Rules For Businesses

Pennsylvania Senate Rejects Bill to Create Cannabis Control Board

ANOTHER STEP TO LEGALIZATION? NORMALIZATION? MD GOVERNOR MOORE HISTORIC PARDONS OF THOUSANDS;

REDMAN GETS BLUNT WITH MONTEL

Anti-Rescheduling Parties Ask Court To Stay Schedule III Cannabis Order

Shining a spotlight on compliance and innovation at Cannabis Expo Johannesburg 2026

Village Farms CEO Explains $15 M Raise + The CMS CBD Pilot

“Our system can manage equipment across 10,000+ m² using just a few wires”

Florida Workshop to Discuss What Constitutes a ‘Cartoon’ in Hemp Packaging

Mazar-i-Sharif Hash Wednesday

Afghan Black Hash Wednesday

Weak Michigan Cannabis Sales Again in July – New Cannabis Ventures

From Finance to Wellness: Brad Zerman’s Impactful Pivot

DEA’s Cole Reverses His “priorities” ; Prohibitionists Dig In; Dead & Co Celebrates 60 years in SF

Re-release of the full show of Cannabis Coast to Coast news. Republican Texas DA Fires Up vs. laws;

Your Cannabis Business: Consistent Filings Are Critical

Curaleaf Q2 Revenue Falls 8% – New Cannabis Ventures

-

Cannabis News10 months ago

Cannabis News10 months ago“Our system can manage equipment across 10,000+ m² using just a few wires”

-

Florida10 months ago

Florida10 months agoFlorida Workshop to Discuss What Constitutes a ‘Cartoon’ in Hemp Packaging

-

Video8 months ago

Video8 months agoMazar-i-Sharif Hash Wednesday

-

Video8 months ago

Video8 months agoAfghan Black Hash Wednesday

-

aawh10 months ago

aawh10 months agoWeak Michigan Cannabis Sales Again in July – New Cannabis Ventures

-

Video10 months ago

Video10 months agoFrom Finance to Wellness: Brad Zerman’s Impactful Pivot

-

Video10 months ago

Video10 months agoDEA’s Cole Reverses His “priorities” ; Prohibitionists Dig In; Dead & Co Celebrates 60 years in SF

-

Video10 months ago

Video10 months agoRe-release of the full show of Cannabis Coast to Coast news. Republican Texas DA Fires Up vs. laws;